Your City Has an Impact on Your Student Loans

Graduating and deciding where to live is an exciting, big step.

There are many aspects to consider when picking a city to live in. It needs to match your lifestyle, including weather, career opportunities, family ties, and… finances.

For many recent graduates, there’s a practical layer underneath choosing where to live: how far your paycheck will go once student loans and other expenses enter the picture.

Two people earning the same salary can experience completely different financial situations depending on the cost of living in their city. Rent, taxes, transportation, and everyday costs can add up to hundreds or even thousands of dollars each month.

In this article, we break down how different cities can impact your ability to manage student debt, and what to look for when comparing locations. Why the Cost of Living Matters for Student Loan Repayment

Where a graduate lives after school directly affects how manageable student loan repayment becomes. Even with a strong starting salary, housing costs, taxes, and other expenses can reduce the income left to pay down debt.

The Real Cost of High-Rent Cities on Your Loan Budget

Rent is one of the largest monthly expenses, and it varies significantly across the United States. In high-cost cities like New York or San Francisco, rent alone can consume a substantial share of monthly income. For example, according to the real estate company Zillow, the average rent in San Francisco is around $4,250 per month, though many listings are priced above $5,000, depending on unit type and location.

When a larger part of income is allocated to housing, student loan payments often become an adjustable part of the budget. That can mean making only the minimum payment for a longer period and/or delaying additional principal payments. Over time, this can extend your repayment timeline and increase total interest paid.

Salary vs Cost of Living: The Ratio That Actually Matters

Salary alone does not determine financial stability in a given city.

A lower salary in a lower-cost city can sometimes result in higher disposable income than a higher salary in a higher-cost area once rent, taxes, and daily expenses are accounted for.

To understand how, it helps to compare typical monthly expenses across locations. Let’s look at an example using a cost-of-living calculator:

- Let’s assume Graduate A makes $70,000 per year and lives in Springfield, Illinois. For comparison, let’s assume they are considering moving to San Francisco, California.

- Once adjusted for cost of living using the calculator linked above, Graduate A may need to earn over $100,000 in San Francisco to maintain a comparable standard of living.

How can there be such a significant difference? It’s due to potentially higher local prices for common living expenses and other factors, such as state and local taxes. The graphic below illustrates how housing and other expenses can increase the income required to maintain a comparable standard of living across cities.

Average Expense Comparison: Springfield vs. San Francisco Example

| Example Expenses | Springfield, IL | San Francisco, CA | Difference |

|---|---|---|---|

| Housing | $1,000 | $2,260 | +126% ↑ |

| Transportation | $500 | $755 | +51% ↑ |

| Groceries | $500 | $710 | +42% ↑ |

| Utilities | $200 | $230 | +15% ↑ |

For this reason, comparing salary to a city's cost of living is often more useful than looking at salary alone when evaluating job opportunities.

Taxes, Commutes, and Other Hidden Costs

Beyond salary and rent, several additional factors can meaningfully impact take-home income.

State and local income taxes vary widely across the U.S. and can reduce net income even when gross salaries appear high. It would be impossible to accurately list the tax rate of all 50 states in this article, but this interactive map provides a strong, high-level overview.

Additionally, transportation costs also vary by city and available infrastructure. In some metro areas, limited public transit or long commutes can make vehicle ownership necessary for many residents. Other costs, like tolls and public transit fares, can add a recurring monthly expense that reduces the amount of income available for student loan repayment or other financial goals.

State Income Tax Comparison Example

| City | State | State Income Tax Structure |

|---|---|---|

| Chattanooga | TN | No personal state income tax |

| Indianapolis | IN | Flat income tax: 2.95% |

| Pittsburgh | PA | Flat income tax: 3.07% |

| Des Moines | IA | Flat income tax: 3.80% |

| Raleigh | NC | Flat income tax: 4.25% |

| Madison | WI | Graduated income tax: 3.50%–7.65% |

Other regional cost differences, including groceries, utilities, and insurance, can further influence monthly budgets. While each cost may appear modest on its own, the combined impact can change how far income stretches in a given city.

What to Look for in a Graduate-Friendly City

A “graduate-friendly” city is typically one where entry-level salaries, housing costs, taxes, and long-term career growth are balanced.

Job Market and Entry-Level Salary Ranges

A strong job market is often the starting point for any city-specific evaluation, but entry-level salaries are just as important. Some cities may have a high concentration of jobs, but relatively modest starting salaries that don’t fully offset living costs.

Other metro areas may offer fewer total openings but have higher starting salaries in major industries such as tech, healthcare, finance, or engineering. The strength of a city’s job market is best evaluated by looking at both the availability of entry-level roles and the typical salary ranges for any chosen field.

Average Rent and Housing Costs

Housing costs vary widely due to local economic differences, housing supply, policy, and population. Rather than focusing on a single “average,” it is more useful to compare how rent levels interact with entry-level income in a given city.

In some locations, rent may represent a manageable portion of monthly earnings, leaving room for student loan payments and other goals. In others, housing costs can take up a disproportionate share of income.

This relationship between rent and income is one of the primary drivers of a city's financial sustainability, particularly when student loan repayment is part of the monthly budget.

State Income Tax and Student Loan Deductions

State and local taxes generally reduce take-home pay, which is why understanding the obligations and potential deductions is critical for financial planning.

Some states, like Nevada and South Dakota, impose no state personal income tax, while others, such as California and Hawaii, have comparatively high state income tax rates, which reduces monthly net income.

Beyond taxes, student loan interest deductions may be available for federal tax obligations depending on income level and filing status, though eligibility and benefit amounts vary.

Quality of Life and Long-Term Growth Potential

Beyond financial considerations, quality of life and long-term career opportunities are important considerations when selecting a city.

Living where YOU want to live matters, and it can affect your mental and physical health. At the same time, local job growth matters from a long-term financial standpoint. If a city has a declining or limited industry, it may not be the strongest career move.

Balancing short-term affordability with long-term career development and happiness is paramount when deciding where to build a post-graduation life.

There is no single "best" city for graduates managing student loan debt. Instead, the right city depends on how well salary, housing costs, job opportunities, and overall cost of living balance. As of March 31, 2026, Americans owe approximately $1.7 trillion in outstanding federal student loan debt, held by more than 42 million borrowers.

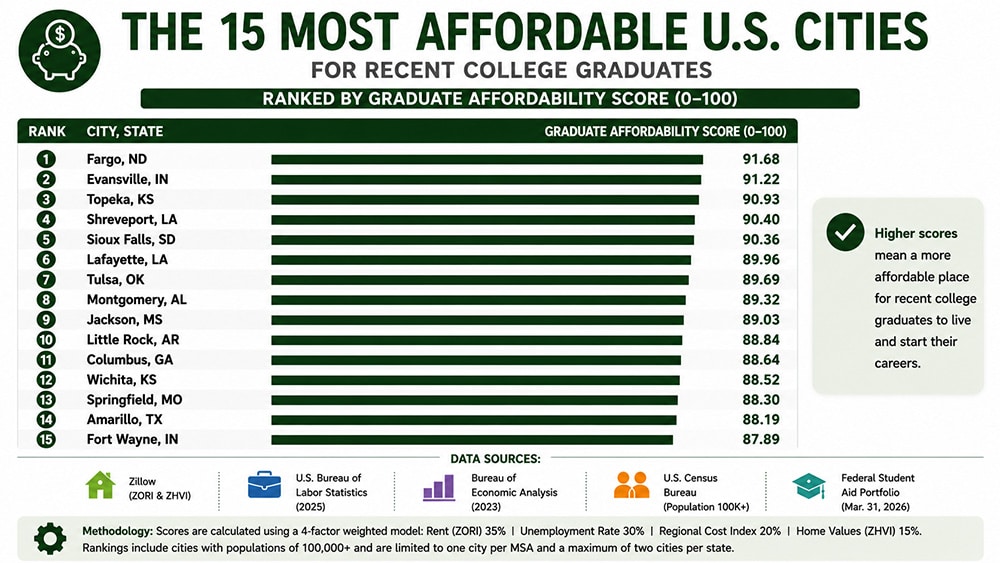

The Top 15 Most Affordable Cities with Strong Job Markets

Low-cost cities are not automatically the smarter financial choice for graduates carrying student loan debt, but they solve a different problem than high-earning cities do.

The trade-off here is less about salary growth and more about how far a smaller paycheck actually stretches once rent, utilities, and everyday costs are factored in. Entry-level salaries in these metros tend to sit below the national average, but so does nearly everything a new graduate has to pay for.

The gap between income and cost of living can mean faster progress on loan repayment, more money set aside in savings, and less month-to-month financial pressure, even without the higher salary ceiling that expensive metros can offer. That trade-off only holds up if the local job market can actually support steady employment.

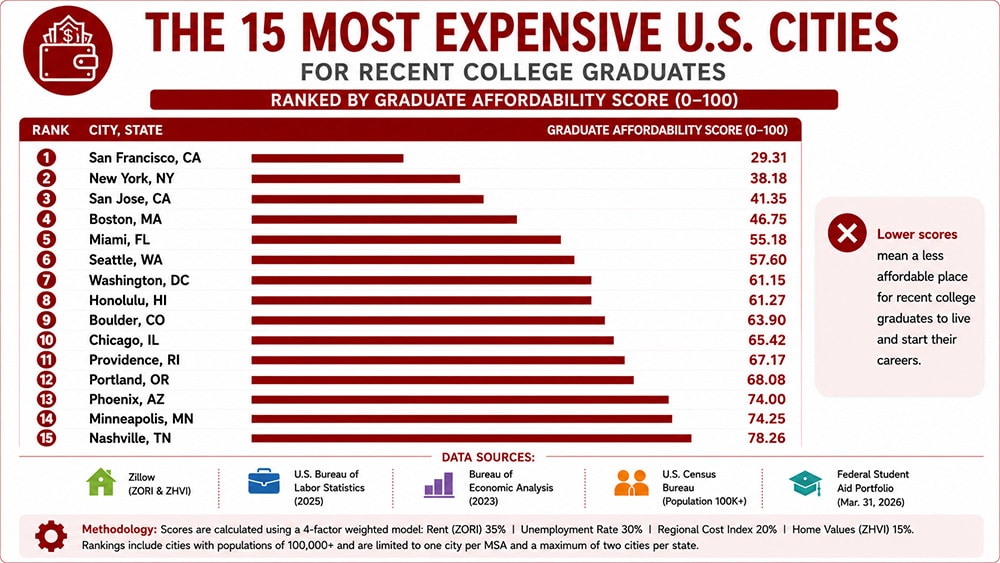

The Top 15 Most Expensive Cities with Strong Job Markets

High-cost cities are not automatically the wrong choice for graduates with student loan debt, but they require a different way of evaluating affordability.

The financial trade-off is less about rent alone and more about whether career growth and salary progression can realistically keep pace with higher living costs. In certain industries such as tech, finance, media, and consulting, high-cost metro areas may offer stronger entry-level salaries and greater access to large employers and professional networks.

Over time, this can lead to a higher earning potential that may offset the initial cost-of-living gap. However, this balance depends heavily on the field and early-career trajectory. If salary growth is slow or inconsistent, higher housing and transportation costs can significantly limit progress toward student loan repayment, savings, and other financial goals.

How to Evaluate any City for Your Situation

Every city comes with different tradeoffs, and what works for one graduate may not work for another. Opinions from family or friends can be helpful, but they are often shaped by personal preferences and circumstances that may not match your situation or priorities.

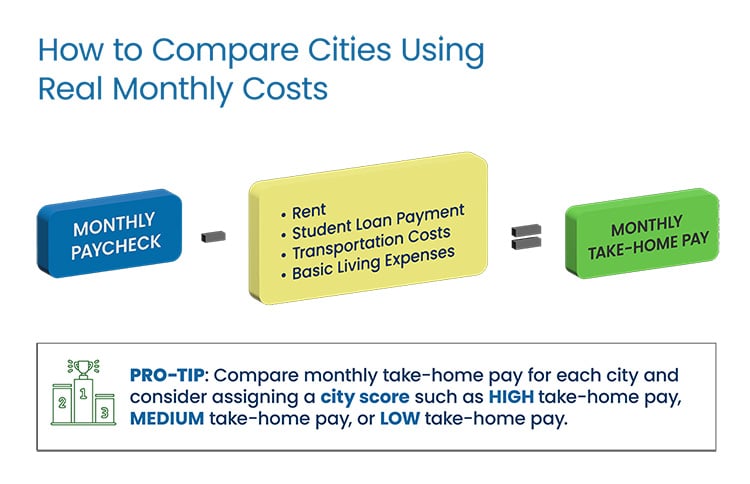

Building a Personal Cost of Living vs. Loan Payment Calculator

A practical way to compare cities is to treat it like a monthly breakdown rather than a lifestyle decision.

Start with estimated monthly take-home pay, then subtract:

- Rent

- Student loan payment

- Transportation (car, insurance, gas or public transport costs)

- Basic living costs (groceries, utilities, entertainment, healthcare)

What remains is the amount of flexibility in your monthly budget. A key comparison to note for each city is how much income is left after fixed expenses.

Questions to Ask Before Accepting a Job Offer in a New City

Before accepting a job offer (or moving without one), try writing down answers for the following questions:

- After rent and expenses, what is my monthly take-home pay?

- Does my remaining budget have room for student loan payments or savings?

- Can I expect salary growth? If so, what percent per year?

- Does commuting require a car or the use of public transport? What are the estimated monthly costs?

- Can I be happy anywhere else?

These simple questions help reveal how feasible it will be to thrive in any city once real expenses are accounted for.

Reducing Your Student Loan Burden Regardless of Where You Live

Location can influence how manageable student loan repayment feels, but repayment strategy also matters. Sometimes, adjusting repayment terms or lowering monthly payments can provide additional flexibility, regardless of where you live.

Income-Driven Repayment Options for Federal Loans

Federal student loan borrowers may have access to Income-Driven Repayment (IDR) plans, which adjust monthly payments based on income and family size. Depending on eligibility, these plans can reduce monthly payment obligations.

Some IDR plans also include forgiveness provisions after a required number of qualifying payments, subject to current federal rules, eligibility, program availability, and potential tax implications.

Borrowers considering federal repayment changes should review current Department of Education guidance and the Student Loan Simulator before selecting a plan. Yrefy also published an article on our blog about multiple repayment options for both federal and private student loans.

Refinancing Private Student Loans for a Lower Monthly Payment

Private student loans operate differently from federal loans and do not include federal repayment protections or forgiveness programs.

In some cases, refinancing may help lower monthly payments by extending repayment terms or securing a lower interest rate, depending on credit profile, income, and lender eligibility requirements. Lower monthly payments can improve cash flow and make higher-cost cities more financially manageable.

Borrowers should carefully review student loan refinancing terms, total repayment costs, interest rates and eligibility requirements before making changes to existing loans.

How to Make Your Loan Work for Your City

Every city comes with different financial pressures.

In some locations, housing costs may be the primary challenge, while in others transportation, taxes, or limited career opportunities may have a larger impact on monthly budgets.

This does not mean you should automatically live in the cheapest city possible. Take time to really run the numbers, consider your personal and professional goals, and try to find a city that mixes preferred lifestyle with smart finances.

Next Steps and Final Considerations

Where a graduate chooses to live is an important personal and financial decision.

For some borrowers, a lower-cost city may create more opportunities for savings or faster loan repayment. For others, a higher-cost city may make sense if long-term career growth makes up for the added expenses.

Wherever you land, a lower monthly payment can make any city more livable.

If delinquent or defaulted private student loans are limiting your financial flexibility, Yrefy may be able to help. Yrefy works with borrowers who may not qualify for traditional refinancing, including those with bad credit (eligibility requirements and terms apply).

To learn more, contact us at (866) 816-7649 or fill out our contact form on Yrefy, and a member of the team will reach out.

Disclaimer:

This article is for informational purposes only and should not be considered legal, tax, or financial advice. Please consult a qualified financial advisor or tax professional regarding your specific student loan situation.

Methodology:

Average Federal Student Loan Balance is shown for informational purposes only and was not included in the Graduate Affordability Index. Because the U.S. Department of Education reports federal student loan balances at the state level rather than by city, each city reflects the average outstanding federal student loan balance for its state.

Sources:

Zillow Research Methodology (ZORI/ZHVI)

BLS Local Area Unemployment Statistics Overview

BEA Regional Price Parities Methodology