Our Frequently Asked Questions

Yrefy, LLC is a student loan lender specializing in refinancing distressed and defaulted private student loans. We negotiate with the original lenders and agencies to help our borrowers refinance their student loans. On average, our borrowers reduce their monthly payments by 50%.

Can Yrefy refinance my high-interest rate private education loans, if I have poor credit?

YES! Yrefy is not your traditional lender; credit decisions are not made based on your credit score. Yrefy understands that delinquent or defaulted private education loans can negatively impact your credit score. Therefore, we look at other factors unique to each borrower’s and co-borrower’s financial situation, and we refinance borrowers with bad or low credit scores.

- A fixed interest rate remains the same throughout the life of the loan. This means that once you refinance, your new loan interest will not change.

- A variable interest rate may fluctuate over the life of the loan.

100% of Yrefy private student refinanced loans are fixed-rate loans with the same monthly payment.

Why do I owe more on my private loan today, even though I’ve been making payments?

This is what happens when your monthly payment, doesn’t cover the interest your loan is accruing. This is due to a reduced payment program. This results in the loan's principal increasing each month, even while you are making payments. This is referred to as Negative Amortization, or Neg-Am.

What repayment terms are available?

Yrefy offers flexible private student loan refinance options to potential borrowers based on the loan balance to be refinanced:

- 3-year to 20-year repayment plan with fixed interest rates at 0.1 - 5.99% APR.

- 20-year repayment plan is at the discretion of the Yrefy.

- Fixed interest rates will vary based on loan amounts and meeting eligibility requirements.

- Use our student loan refinance calculator to compare your current student loan to a new Yrefy loan.

Is there a formal hardship forbearance policy?

Yrefy offers an incentive program, SKIP-12 Program, for borrowers that are experiencing temporary hardship. Borrowers who qualify can skip 1 payment, every 6 months, for the life of the loan.

Another option, Yrefy will work with our borrowers to refinance their loan, extending the payment term, if a lower payment is needed for the borrower success long-term.

Or are called on active military duty?

You can pause payments, due to Military deployment. Yrefy will issue a forbearance based on the Military Lending Act may be granted in 12-month periods. There is no time limit for this forbearance but must be renewed annually.

Are there any application or origination fees?

- No application fee.

- Yrefy will assess Borrowers, nominally, a 5% loan origination fee, at the time of loan payoff on the total Private Education Refinance, based the refinances amount.

Is there a penalty for early loan payoff?

There are no prepayment penalties.

Can I release my co-borrower?

Yes, making consistent on-time payments can eventually lead to a co-borrower release.

Does Yrefy check my credit?

A soft credit check is done for prequalification, which does not hurt your score, but a hard credit check is required for final application.

How does this improve my credit?

By replacing a defaulted, delinquent loan with a new, active loan that is paid on time, you can rebuild your credit score.

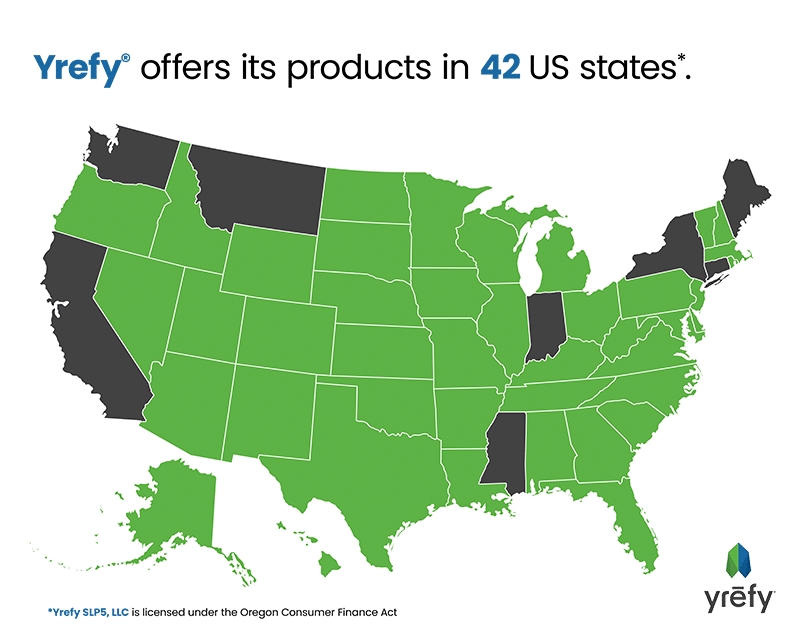

What states does Yrefy offer services in?

Yrefy currently offers refinancing in 42 states within the United States. States we provide services in are: Alabama, Arkansas, Arizona, Colorado, District of Columbia, Delaware, Florida, Georgia, Hawaii, Iowa, Idaho, Illinois, Kansas, Kentucky, Louisiana, Massachusetts, Maryland, Michigan, Minnesota, Missouri, North Carolina, North Dakota, Nebraska, New Hampshire, New Jersey, New Mexico, Nevada, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Vermont, Wisconsin, West Virginia, Wyoming.

How do I apply?

Borrowers can contact Yrefy for a personalized, in-depth consultation regarding their loan situation. Call us at (866) 816-7649 or fill out our contact us form.

More About Yrefy?

About Us

Learn more about Yrefy. Our story, mission, and values that make us different compared to traditional lenders.

Our Team

Learn more about our team and the people committed to helping you move forward.

Testimonials

Read or watch our customer testimonials of why they chose Yrefy and how we helped them.

Reviews

Yrefy has received many reviews from past customers. We have a 4.8 star rating on Google.

Press & News

Yrefy has been reviewed, featured on, and endorsed by many large news and financial websites.